flow through entity canada

Types of flow-through entities. Flow-through limited partnerships are valuable to investors who have current income that will be taxed at the highest marginal rate.

Business Income And Business Taxation In The United States Since The 1950s Tax Policy And The Economy Vol 31 No 1

Investors buying into flow-through entity limited partnerships are able to deduct 100 or more of their investment against income by the end of the.

. Flow-through LPs offer tax benefits to investors similar to flow-through shares but they have some different features. There are three main types of flow-through entities. These tax benefits flow through to investors in the fund.

The flow-through share entered the Canadian tax code just over 25 years ago. Where a single member LLC is owned by a non US. In Canada however investment corporations whether mortgage trust mutual fund or partnership are regarded as flow-through entities.

For more information concerning the processing of the forms you may contact the Business Returns DivisionCall 1-855-432-5517. A pass-through entity also called a flow-through entity is a type of business structure used to avoid double taxation. An LLC is a type of entity that is offered in the US and for US tax purposes is a flow through entity.

Trade or business of a flow-through entity is treated as paid to the entity. Flow-through LP units may be issued by an entity that purchases a diversified portfolio of flow-through shares. Amounts renounced to the partnership which can be allocated to the partners.

This rule applies for purposes of Chapter 3 withholding and for Form 1099 reporting and backup withholding. There are several advantages of flow-through entities that investors should take advantage of. A foreign partnership.

An investment tax credit ITC on flow-through mining expenditures for individuals. This section provides information on the types of investments that are considered flow-through entities and how to calculate the capital gain and loss resulting from the disposition of shares of or interests in a flow-through entity. Again the earnings of the LLC are flowed through to the ultimate owners of the LLC for US tax purposes.

Looking back mining executives lawyers bankers and accountants believe this quirky Canadian tax innovation has generated billions for mining exploration and contributed to the development of some of the countrys most notable mines such as the Ekati and Diavik. Typically businesses are subject to corporate tax while business owners also have to pay a personal income tax. Though ULCs are taxed as corporations in Canada they are eligible for check-the-box election in the United States and may be taxed as either a corporation or a flow-through entity.

An entity in which partners are not personally liable for the companys debt obligations. Advantages of Flow-Through Entities. Flow-through shares FTS can provide mining companies with reduced-cost access to financing in this situation.

Deductions from income through renounced expenses. To help clarify this issue this document also includes a practical and detailed example of a publicly traded Canadian mining entity involved in issuing flow-through shares to investors. S corporation S corp.

These entities are generally used by foreign investors to gain advantageous tax treatments in their home jurisdiction. Person or entity new regulation 3017701-2 c 2 vi A classifies these entities as corporations. This triggers Internal.

Tax purposes and accordingly its operations are reported on the members individual tax return. Flow-through entities are a common device used to limit taxation by. The information in this section also applies if for the 1994 tax year you filed Form.

The basic principle behind flow-through shares which are unique to the resource sector in Canada is that a mining corporation willing to forego the tax benefit of certain CEE and CDE amounts that it incurs can renounce. Flow-through shares have helped expand Canadas resource sector since their introduction to the Canadian tax system in 1954. A business owned and operated by a single individual.

Limited liability corporation LLC. In general to take advantage of these benefits investors need to hold the funds for a fixed period usually 18 months to two years. Downsides to Flow-Through Entities There is a criticism on the flow-through entity this resulted from one of its drawbacks in which owners of entities are taxed on the income not directly receive by them but by.

Income that is or is deemed to be effectively connected with the conduct of a US. FTS investors may benefit from. Unlike flow-through shares where only the original investor can deduct renounced expenses the.

Corporate subsidiary Corporation form rather than flow-through form Most provinces and territories and federal corporations require initial registration as well as annual filings with Corporations Canada if a federal corporation and in the province or territory where the corporation is incorporated or registered. A flow-through entity is a legal business entity that passes income on to the owners andor investors. Calgary 587-475-3766 Vancouver 604-666-8430 Rouyn-Noranda 438-357-1013.

At that time the Canadian government introduced provisions to allow for. When a business entity is treated as a flow-through entity it means that the businesss profits will not be taxed twice. Accounting for flow-through shares with attached share purchase warrants.

Flow-through shares FTSs For technical information concerning the FTS program you may contact the following tax services offices. This is definitely a factor that American businesses need to consider if they want to do business in Canada through an LLC. Flow-through shares FTSs On July 10 2020 the Government of Canada announced changes to protect jobs and safe operations of junior mining exploration and other flow-through share issuers by extending the timelines for spending the capital they raise via flow-through shares by 12 months.

To avoid this a company may be registered as a pass-through entity so that the revenue earned is taxed as. Individuals excluding trusts can claim a 15 non-refundable ITC for certain mining CEEs. A form of LLC in which ownership is limited to certain.

All of the following are flow-through entities. This is important because a company that is taxed twice will simply not be able to develop. A single member LLC is considered a disregarded entity for US.

On December 16 2020 the Department of Finance.

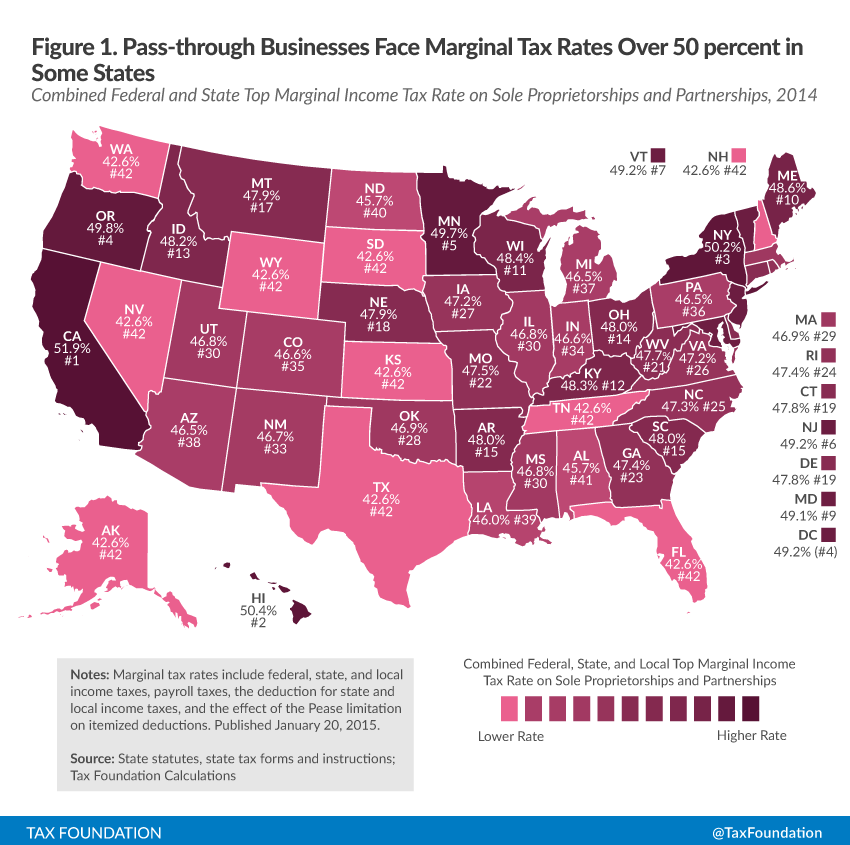

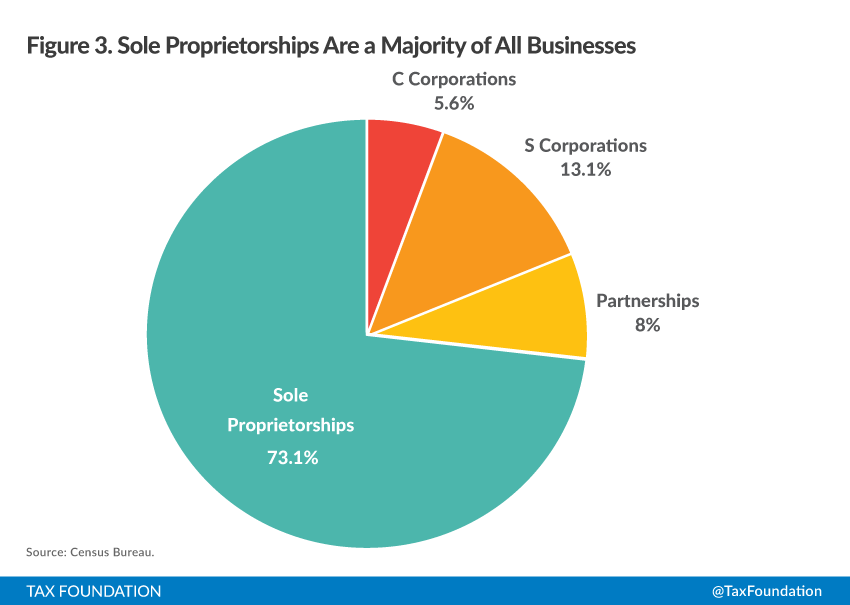

An Overview Of Pass Through Businesses In The United States Tax Foundation

An Overview Of Pass Through Businesses In The United States Tax Foundation

An Overview Of Pass Through Businesses In The United States Tax Foundation

The Drug Review And Approval Process In Canada An Eguide

Considerations For California S Pass Through Entity Tax Deloitte Us

Business Income And Business Taxation In The United States Since The 1950s Tax Policy And The Economy Vol 31 No 1

2

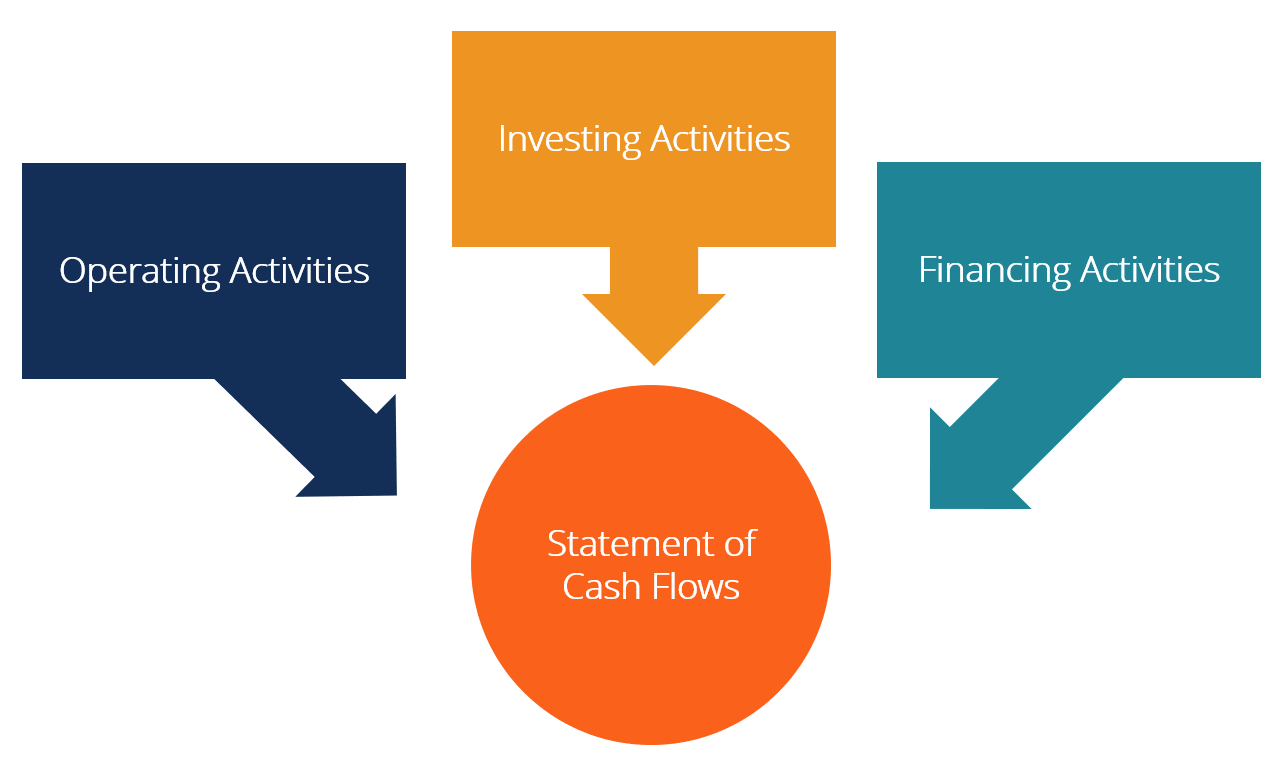

Statement Of Cash Flows How To Prepare Cash Flow Statements

Business Income And Business Taxation In The United States Since The 1950s Tax Policy And The Economy Vol 31 No 1

Considerations For California S Pass Through Entity Tax Deloitte Us

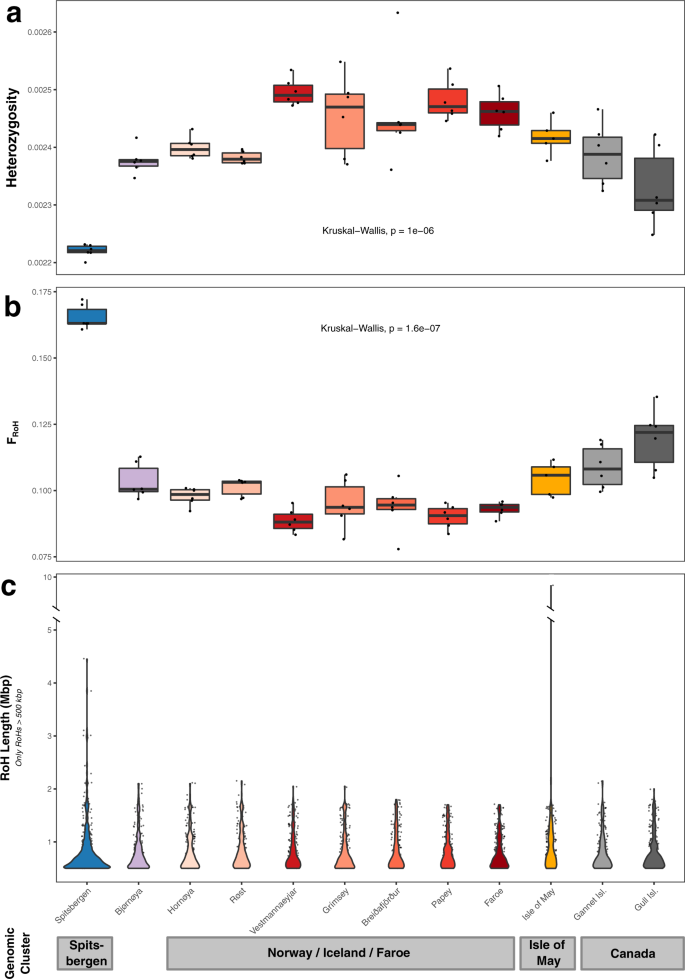

Complex Population Structure Of The Atlantic Puffin Revealed By Whole Genome Analyses Communications Biology

Federal Register High Wage Components Of The Labor Value Content Requirements Under The United States Mexico Canada Agreement Implementation Act

Considerations For California S Pass Through Entity Tax Deloitte Us

Cash Flow Guide Deloitte Us

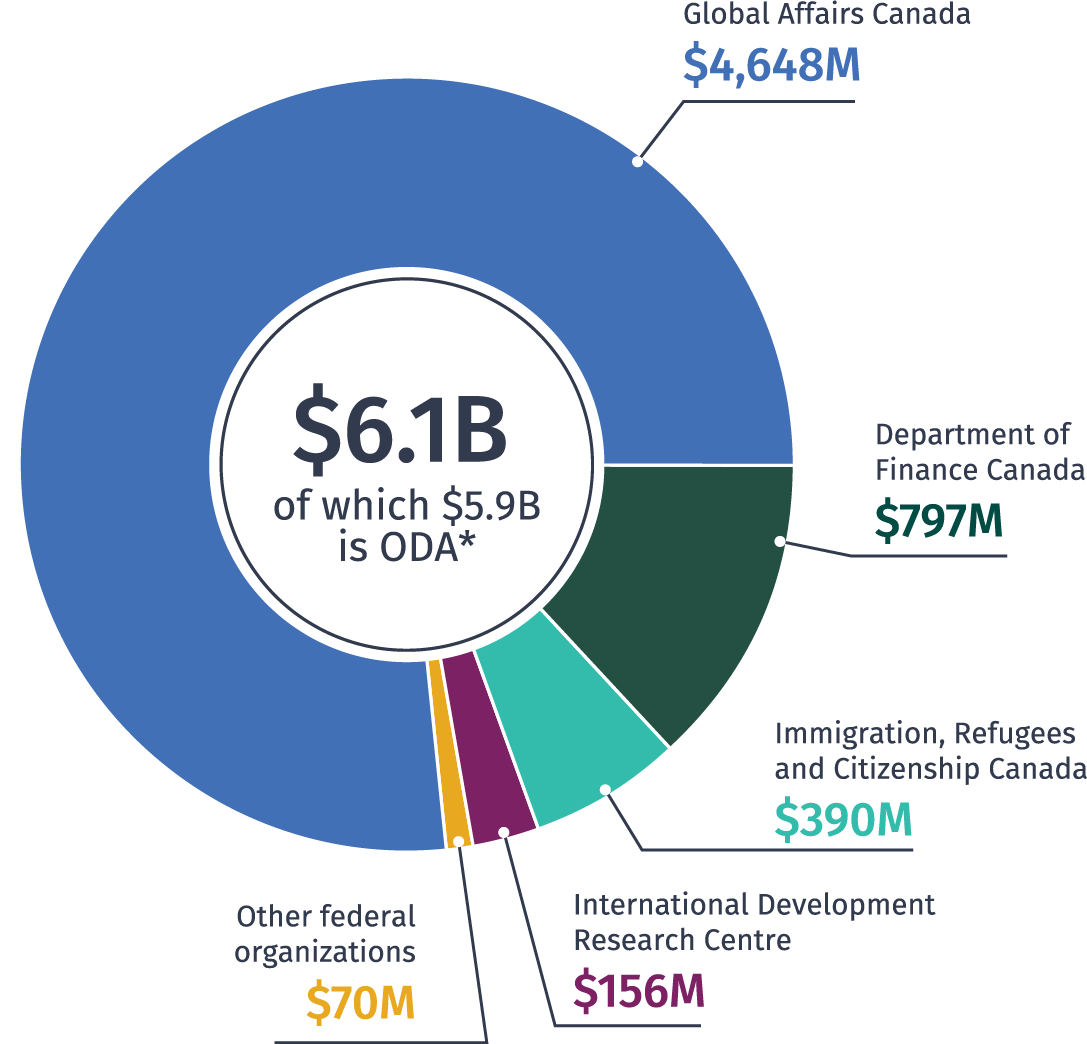

Report To Parliament On The Government Of Canada S International Assistance 2018 2019

Complex Population Structure Of The Atlantic Puffin Revealed By Whole Genome Analyses Communications Biology

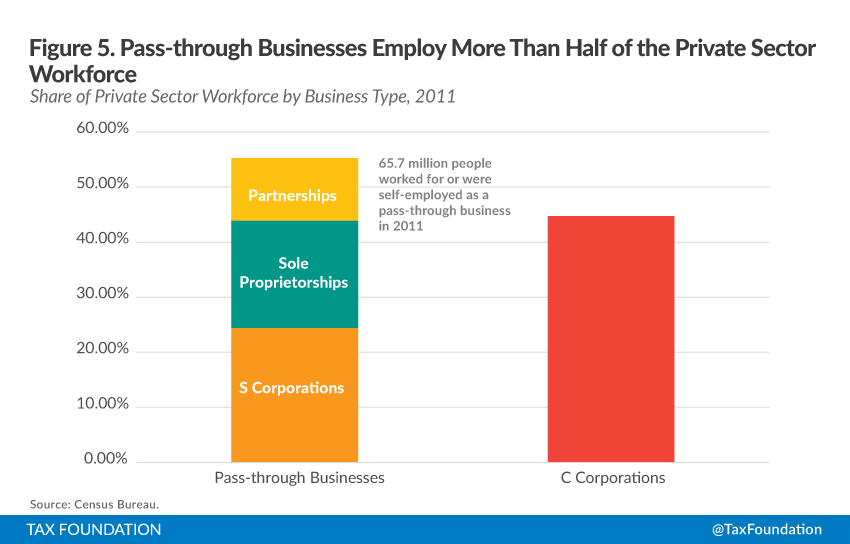

An Overview Of Pass Through Businesses In The United States Tax Foundation

An Overview Of Pass Through Businesses In The United States Tax Foundation

An Overview Of Pass Through Businesses In The United States Tax Foundation